For many CFOs, blockchain still sounds like a crypto topic.

But in trade credit insurance and trade finance, the real opportunity is not speculation. It is about solving a very practical problem: creating a trusted digital record for insured receivables.

That matters now because the regulatory environment is moving. The U.S. Senate Banking Committee is scheduled to consider the CLARITY Act on May 14, 2026, a major step in the U.S. debate around digital asset regulation. The bill has not yet become law, but the fact that it is moving through the banking committee shows that digital asset infrastructure is entering a more serious phase.

For insurers, banks, brokers and corporates, this is the moment to ask a simple question:

If trade finance becomes more digital, who will own the trusted infrastructure?

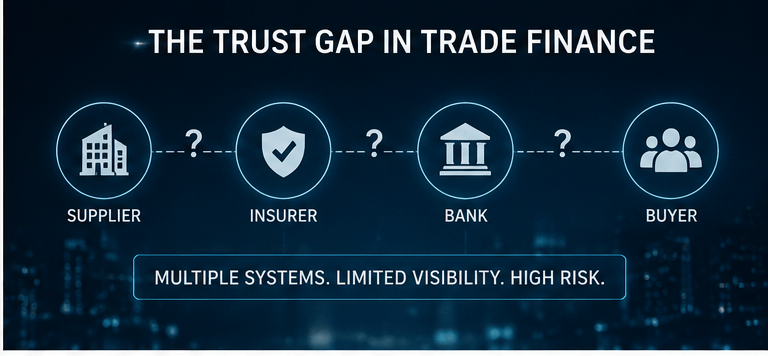

The problem: insured receivables are still difficult to finance

Trade credit insurance already plays a critical role in global trade. It protects suppliers against buyer default and gives banks more comfort when financing receivables.

But the process is still highly document-based.

A bank financing an insured receivable needs to know:

Is the receivable real?

Is it covered under the policy?

Has it already been assigned or financed?

Has the policyholder complied with the insurance obligations?

Who has the right to receive payment or an insurance claim?

These questions are often answered through emails, PDFs, ERP exports, insurer confirmations and manual checks.

That creates cost, delay and risk.

The two big risks for banks

The first risk is double financing.

A company may use the same receivable to obtain financing from more than one bank. Bank A finances the invoice, but Bank B may later finance the same receivable because it cannot see that it has already been assigned.

The second risk is insurance invalidity.

A receivable may appear to be insured, but the cover may not respond if the policyholder has failed to comply with policy obligations. For example, the company may have missed overdue reporting deadlines, exceeded agreed payment terms, continued deliveries after a buyer limit was reduced, or failed to notify the insurer correctly.

For a financing bank, this is critical. The bank may believe it is financing an insured receivable, but later discover that the insurance protection is no longer valid.

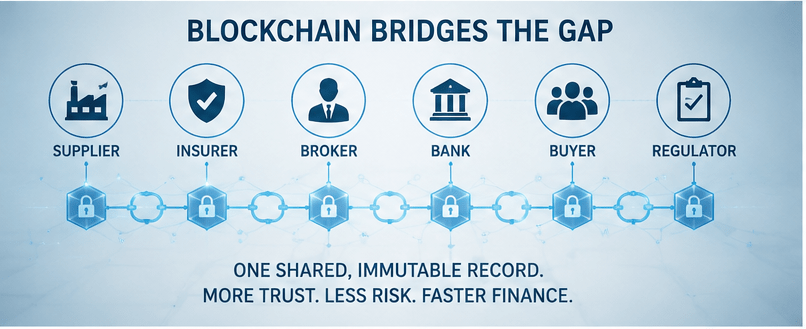

Where blockchain adds value

A blockchain can act as a shared digital registry.

Not a public database of invoices. Not a crypto coin.

A permissioned registry where authorised parties can verify the status of an insured receivable.

For example:

This receivable exists.

It is covered under Policy X.

The buyer limit is available.

Policy obligations are currently complied with.

It has not yet been financed.

It has now been assigned to Bank A.

It cannot be financed again by Bank B.

That is the practical value.

Blockchain can create a trusted status layer between the corporate, insurer, broker and financing bank.

Why this matters for CFOs

For CFOs, the benefit is simple:

Receivables become easier to finance.

If banks can trust that a receivable exists, is insured, has not already been financed and remains compliant with policy obligations, they can provide liquidity faster and with more confidence.

That can mean:

- faster access to working capital,

- less manual documentation,

- lower fraud risk,

- stronger bank confidence,

- potentially better financing terms.

This is not about replacing trade credit insurance. It is about making insured receivables more bankable.

Why this matters for insurers

For credit insurers, the opportunity is bigger than simply providing a policy.

Insurers already sit at the centre of trade risk. They know the buyers, set the limits, monitor exposures and define the conditions under which cover applies.

A digital receivables registry could allow insurers to become part of the infrastructure behind trade finance.

They could provide digital confirmation of:

- policy status,

- buyer limit availability,

- cover percentage,

- compliance with policy obligations,

- assignment status,

- claim eligibility.

That creates value for banks and corporates — and potentially new revenue streams for insurers.

The first-mover advantage

The CLARITY Act is not a trade finance law. But its progress is a signal.

Digital asset infrastructure is moving from the experimental phase into the regulated financial system. Banks, insurers and corporates that wait until everything is fully mature may find that the most valuable infrastructure positions have already been taken.

The first movers will have the chance to define:

- the data standards,

- the registry model,

- the role of insurers,

- the role of banks,

- the rules for assignment,

- the verification process,

- and the economics of the platform.

In trade finance, trust is infrastructure. Whoever builds the trusted digital layer first may gain a meaningful advantage.

A simple example

A company sells €1 million of goods on 90-day payment terms.

The receivable is covered by trade credit insurance up to €800,000.

A bank checks the digital registry and sees:

- the receivable is registered,

- the buyer limit is valid,

- the policy is active,

- no overdue reporting deadline has been missed,

- the receivable has not been financed before.

The bank finances the receivable.

The registry is updated:

Assigned to Bank A.

If another bank later checks the same receivable, it sees that it is no longer available.

If the buyer later defaults, the bank can also see whether the relevant policy obligations were met and whether the insurance claim route remains valid.

That is how blockchain creates value: not by turning invoices into crypto assets, but by turning uncertain documents into verifiable digital records.

Conclusion

Trade credit insurance protects the receivable.

Trade finance monetises the receivable.

Blockchain can verify the receivable.

That is why this topic should matter to CFOs now.

As regulation moves closer to clarity, the opportunity is not to wait for the perfect future. The opportunity is to start building the trusted digital infrastructure that trade finance has been missing for decades